Nothing has dominated recent music news (at least not since the passage of the Music Modernization Act) as much as Spotify’s decision to appeal the findings of the Copyright Royalty Board, or CRB. The move prompted backlash from music publishers and a rebuttal from Spotify, but the actual facts of the debate are buried under piles of legalese.

But the debate here is an important one — not only because of the amount of money involved, but because it illustrates a lot about how the music industry and streaming businesses work (or don’t). While we won’t know the specific legal arguments until the first round of briefs are filed on Friday, we can get a sense from the CRB’s decision (and the opinion of one dissenting judge) for what some of the high-level points will be.

So what’s really going on, what’s at stake, and what should songwriters and consumers look for going forward?

What is the CRB?

The Copyright Royalty Board is a panel of three judges that sit in a special office within the United States Copyright Office. These judges are empowered to set the price for a specific kind of license needed to stream music. (There’s a long and complicated story — political and economic — behind why the government gets to set the price for this license, but it’s enough for now to know that the CRB has the legal power to dictate the prices when the parties can’t come to an agreement.)

The CRB has the ability to set prices only in very specific circumstances. The license at the heart of the current dispute apply to what the law calls a “musical work.” If that seems a little vague, think of it this way; a musical work is what you get when you print a song out in sheet music. It is the composition underlying a performance. By contrast, the law calls the recording of a performance — the work of a singer, band, or other recording artist — the “sound recording.” Musical works (written versions) and sound recordings (recorded versions) are two separate things under copyright law, even if they often show up in pairs.

So where does the CRB come in? The CRB sets the price for a specific type of licenses, known as “mechanical” licenses, for musical works. Mechanical licenses allow a streaming service, like Spotify, to reproduce and distribute the musical work.

The CRB sets rates for five-year periods. Here are the CRB’s rates for 2018-2022. (The proceeding ran long, so even though it was finalized in 2019, the rates included 2018 as a start date.)

What kinds of licenses do services need to stream music, and how does the CRB fit in?

If you don’t know what to make of these categories, don’t sweat it for now. We’ll explain each of them as we go. First, though, a primer on music licenses.

Music copyright is complicated, to put it mildly. Here are the most basic things you need to know:

(a) There are two copyrights in every recorded song—one in the actual recorded track (called the “sound recording”) and one in the underlying composition (called the “musical work”).

(b) Each of these copyrights is a bundle of smaller sub-rights that are held by different people, companies, or entities. These sub-rights cover different uses of the track or composition, so what license you might need (and who you need to pay) varies depending on what you plan to do with the song.

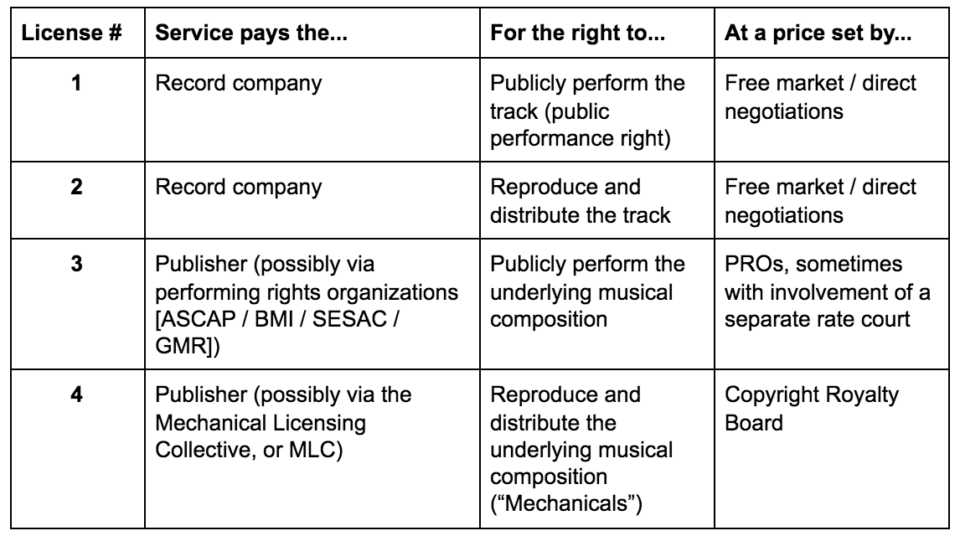

So to stream a single track, a service has to piece together licenses that cover what it plans to do with the song. For your average streaming company, this means acquiring (read: paying for) four separate licenses in order to play nearly every single song for audiences.

If this looks like a lot, you’re not wrong. This is actually a ridiculously simplified version of how payments go; each category is, in reality, riddled with exceptions (sometimes #3 gets paid directly to the songwriter or publisher) and procedural detours. It also doesn’t include the licenses you need to synch music to a video; those are a totally separate beast, and are becoming more and more prevalent as video becomes the big delivery mechanism.

And if you think this chart as it stands is more than a little absurd, well, you’re also not alone; copyright legislation for the last hundred or so years has been one continual process of duct-taping new rights onto old ones, with rights and sub-rights multiplying like amoebas in a petri dish. (Did you know that vessel hulls get copyright protection, for some reason? I don’t understand it either; don’t @ me.)

Back to music. If you’re an interactive streaming music service, you (generally) need, all four of these licenses are needed to stream a single track. (Because copyright is delightful, there’s a slightly different set of rules for non-interactive services. Also terrestrial radio. And legacy/pre-1998 subscription services. Yay!) But as far as you need to know or care, for the purposes of this blog post — if any one of these licenses is missing, the relevant track must disappear from the license-less service, or that service risks liability for copyright infringement.

Okay. So.

Now, see that column of who gets paid? Thanks to our inelegant, not-at-all-intuitive copyright law, each and every one of those entities has a (potentially) very valuable, separate good. And, like any rational economic actor, those entities wants to maximize the amount of money they can extract from the streaming service. Streaming services, by contrast, want to pay the lowest possible price for those goods. But the fact that each license price is set differently means that things get very complicated, very quickly. So, if you’re a service, you’re negotiating for four different products, in three separate forums, against at least two different entities, against the backdrop of three different procedures — and none of these entities or procedures have to acknowledge any of the others. Because each of the license-holders is competing for the same pot of money (the streamer’s revenues), they are, in a way, competing against each other, but they don’t have to (and can’t, under antitrust law) coordinate directly with each other to do so. This means that fights over streaming services licenses occasionally end up being a proxy for fights between different rights holders over how revenue is split.

Meet Streamy

So we have a copyright system that breaks out rights into tiny bundles, a streamer that now has to reassemble those bundles, and holders of those bundles who are all jockeying over for a bigger slice of the same limited pie. Sound like fun yet?

To illustrate how this all works, let’s use a fictional example. Meet Streamy.

Streamy is a music delivery service that offers songs for stream or download, all for $99.99 a year. Go Streamy.

Now, the important thing here is that Streamy — and its numbers — are fictional. The music and streaming industries are notoriously secretive about their financials, and so we legitimately don’t know how much money is changing hands and where. I’ve noted where the numbers have some basis in reality, but for the most part, these are numbers I picked for the sake of easy math.

Streamy takes in about $5 billion in revenue in 2018. That’s a lot of money! But, like most streaming services in the real world — and like Spotify, until very recently — Streamy still isn’t turning a profit. Every dollar that it takes in goes back out in the form of licensing fees, technology outlays, healthcare and salary costs for its employees, advertising, and so on. Of that $5 billion, about $3 billion goes to licensing costs. (It’s worth noting that, as far as we can tell, this is actually much better than most real streaming services make out; most either have a larger company [Apple, Google, Amazon] backing them or subsist on round after round of investment capital [Spotify].)

Streamy and slicing up the (very tiny example) pie

There’s an important dynamic at play here; the competing (and often conflicting) claims of rightsholders. To illustrate this, consider the following hypothetical.

Imagine Streamy wants to play only one song, and has $1 to spend on licensing that song. (This is not one of those numbers that has a basis in reality. The numbers here aren’t even important; it’s the underlying principle that matters.) Let’s say Streamy, through some dark magic, has managed to split those licensing fees evenly four ways, with a price of 25 cents for each of the four licenses it needs. That means Streamy pays the record company $0.25 for License #1 and another $0.25 for License #2; pays the PROs $0.25 for License #3; and pays music publishers $0.25 for License #4.

Now, imagine that a bunch of record companies look at Streamy and say, “You know, I think I can charge more for my licenses, even if it means Streamy has to take on some debt.” So the record company doubles the price of its licenses (#1 & 2), up to $0.50 total. Streamy’s bill suddenly jumps from $1 (25 / 25 / 25 / 25) to $1.50 (50 / 50 / 25 / 25). Streamy now has to get that extra $0.50 from somewhere, and if it’s like most streaming services, it’s already spending everything it takes in. Maybe it can negotiate a slightly lower rate for License #3 (with the PROs), but that can trigger a hugely expensive legal battle; and License #4 is set by the CRB for a minimum of five years, so Streamy can’t change that until the time is up, come hell or high water.

The end result is that, even when Streamy only has $1 worth of money to give, it’s got four separate claimants who are all claiming they’re entitled to the exact same penny.

What does the CRB have to do with this?

To its credit, the CRB tries to take this problem of “many uncoordinated claimants scrambling for the same penny” into account. First, it designs its rates not as a flat amount, but as a pair of percentages: one based on the service’s total revenue, and a larger one based on what the streaming service pays in licensing for its content (appropriately known as the “total content cost,” or “TCC”). The streaming service pays whichever option produces the bigger bill.

Second, CRB rates are what’s called “all-in” rates. An “all-in” rate reflects the combined total that a streaming service must pay for licensing musical works via license #3 (mechanicals) and #4 (public performance). All-in rates act as a kind of cap on how much a service has to pay for musical works by locking in the total bill for licenses #3 and 4. If public performance rates go up and eat up more of the “all-in” rate, mechanicals will get cheaper. If public performance rates get cheaper, mechanicals will go up to eat up the difference. And since public performance rates are themselves complicated beasts (some are set by rate courts, others by private negotiation; some are through PROs, others not; etc), this provides some stability for streaming services where they otherwise don’t have much.

Record companies, though, are a free market wildcard.

How much does Streamy owe?

Let’s check back in with the CRB, and the rates Streamy has to pay under the new rulemaking. Remember this?

Streamy has $5 billion in revenues for 2018, and looks like it’s going to make a similar number for 2019. Let’s figure out the total bill under the 2019 rates.

Following the “percent of revenue” calculation for 2019 (12.3 percent), Streamy would owe $615 million for all its musical composition licenses. Because that’s an all-in rate, that $615 million is going to be split in some way between mechanical licenses (#3) and public performance licenses (#4).

Under the TCC calculation, Streamy would owe 23.1 percent of its $3B in content costs, or $693 million. (Again, that $693 million is going to be split between licenses #3 and 4, so it’s not all going to mechanicals.) Since that’s the bigger number, that’s Streamy’s bill. And unless Streamy’s revenue grows way faster than its licensing costs (not very likely in the current market), TCC is going to stay the dominant rate for the foreseeable future.

Where the TCC rate falls apart

Remember that Streamy’s TCC rate is (by definition!) a portion of its total content cost, which includes both the CRB rates and the rates paid to record companies. The CRB rate is a fixed number, but the record labels are a free market wildcard; they are completely free to charge whatever they want, under any terms they want. If record companies raise their rates, that drags up the total cost of content, which in turn drags up the TCC-based rate that Streamy owes. Conversely, if record companies cut their rates, the total cost of content goes down, and the CRB rate goes down with it.

Illustrating the problem with this is going to require some math, so buckle in.

Say, for example, that record companies demanded 70 percent of Streamy’s revenue as licensing fees. That’s a big number, but not impossible (at least in the opinion of one CRB judge). In other words, for every dollar in revenue, record companies are claiming 70 cents. The TCC-linked rate for mechanicals is 23.1 percent (0.231 in decimal). Playing out the math:

Record company payment + mechanical rates = Total Content Cost (TCC)

.70(1) + mechanical rates = TCC

Mechanical rates = 0.231*TCC

.70(1) + 0.231TCC = TCC

.70 = 0.769TCC

.91 = TCC

Unglaze your eyes, because this is the important takeaway: A jump in record company rates to 70 percent would not only drag up the mechanical rates with it, it would drive the total cost of content to a point where it consumes over ninety percent of Streamy’s revenue — 70 percent to record companies, and 21 percent in the all-in mechanical rate. That leaves less than 9 percent of Streamy’s revenue to pay for everything we mentioned above. Critically, 21 percent of revenue is well above what the rate would be (12.3 percent) if the service was allowed to calculate using its “percentage of revenue” method.

(This isn’t isolated to extreme examples, either; even more modest record company rates will swell the TCC-based mechanical rate to consume most of a company’s revenue. Setting record company rates at 50 percent drags up content costs to over 65 percent of the streamer’s total revenue, and setting them at 60 percent brings the total content bill to nearly 80 percent of a streamer’s revenue.)

It doesn’t take much to see how this could result in a runaway rate increase, especially when you consider that most major publishers are owned by labels. Although there are some guardrails against coordination, that presents a possible conflict of interest when a record company can nudge its own rates to increase the cash flow to its publisher arm.

In previous CRB rates, there was a cap on the TCC-linked rates specifically to prevent this problem. This round, however, the CRB ditched the cap, and created the risk of a runaway rate.

Conversely — and perhaps counterintuitively — this puts publishers and songwriters at risk, too. If a label and service merge (or buy one another out, or even share major equity stakes), the record company may engage in “sweetheart” pricing — namely, lowering the licensing rate for its affiliated streaming service. This would drive down the total cost of content, and the mechanical rates as a result.

How Record Companies Will React

At the core of the dispute lurks one big question: How will record companies react to all of this?

Publishers and songwriters, advocating for a higher rate for their contributions, asserted that it’s in no one’s interest to completely kill off streaming services; because of this, they argue, record companies will just accept getting a smaller slice of the pie, and nobody will be harmed.

But many industry watchers, and at least one CRB judge, aren’t so sure. Record companies are deadly serious about defending their revenues, and there are a lot of options between “backing off gracefully” and “raiding a service until it dies.” One of the most obvious, and most troubling, is that labels may decide to just buy a controlling stake in a service, and take their payment in equity rather than cash.

The take-away, and what to look for

Right now, we don’t know exactly what Spotify will argue, and who, if anyone, will join them in the appeal — though it seems likely that most of the licensees will. Spotify notified the DC Circuit Court of Appeals that they would be appealing “all underlying orders, judgments, rulings, findings, and determinations” reached by the Board, but didn’t put forward any arguments. (This is standard for administrative appeals, and you shouldn’t read anything into it.) Spotify’s formal arguments won’t be public until their opening brief is due on April 12. Until then, we can only go off of PR campaigns and public statements that don’t neatly translate to legal arguments.

There are a few important things to take away from this mess. The first is that what seems like a really simple act to the end user — streaming a song — is, thanks to our Byzantine copyright law, an insanely complicated proposition, with an incredible number of entities who have the legal right to stop it, get paid for it, or both. Relatedly, you may have noticed that this post — all 3,000+ words of it — doesn’t really talk about artists. That’s because they’re often absent from these negotiations, tucked behind layers upon layers of private companies, publishers, negotiating bodies, and other entities — all of whom take a slice off the top of the royalties before they reach the artist.

Another major point is that consolidation among gatekeepers in the music business can be incredibly dangerous. Three major record labels control 70 percent of the global music market; music publishing (musical works, i.e. songwriter’s market) fares a little better, but is still dominated by three major publishers that together control around 60 percent of the total market. The power of any one player to set the terms of negotiation industry-wide is already incredible. As discussed above, a single large record label upping its licensing rate can have cascading effects on the cost of music across the entire ecosystem. And the same is true for streaming services; the fewer services exist, the greater their negotiating leverage against labels and publishers. Artists are also at risk from consolidation, as a narrow market means fewer choices, lower rates from streamers and publishers, and a greater risk of being locked out or disadvantaged in favor of more popular acts.

Regardless of how this plays out, it’s an important story to follow. We’ll keep you updated.